Should I use my savings to pay off my credit card debt, or continue saving?

If your credit card interest is higher than what your savings earn, paying off your debt is usually the better financial move. But there’s one important exception: You still need a buffer to keep from falling into more debt in emergencies.

This decision isn’t just about maths. It’s about making sure you’re not saving money on interest today, only to land back in debt tomorrow.

The simple rule to start with

Before getting into nuance, here’s a practical way to think about it:

- If your debt interest is high (typically 15–20%+)

- And your savings earn relatively little (typically 3–8%)

Then, prioritising debt repayment will almost always save you money.

But: Don’t use all your savings to do it. Keep a minimum buffer in place.

Why paying off debt usually wins (the maths)

Credit card debt grows fast. Savings grow slowly.

For example:

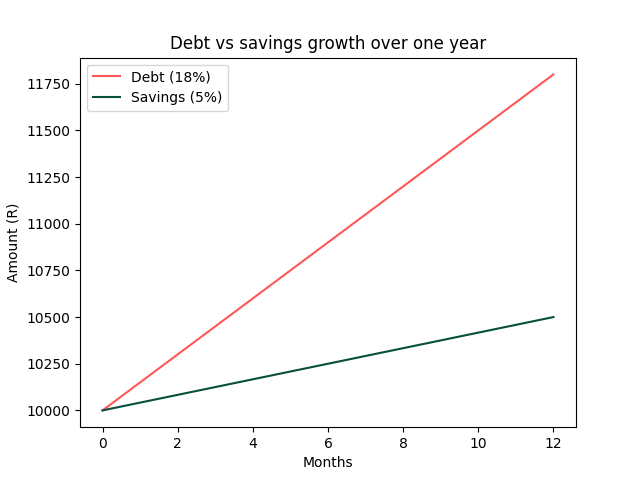

- R10,000 in credit card debt at ±18% interest

- R10,000 in savings earning ±5%

Over a year (simplified):

- Your debt could cost you around R1,800 in interest over the year

- Your savings could earn you around R500 in the same time

So you’re roughly R1,300 worse off by holding both.

This isn’t exact. Actual credit card interest depends on how your balance changes over time. But directionally, the gap is real.

You’re paying a high price to keep money sitting in a low-return account.

Comparing credit card debt vs savings

Where this goes wrong for people

If the maths is so clear, why not just use all your savings to clear the debt?

Because life isn’t predictable. If you wipe out your savings and something unexpected happens, you’re forced straight back into debt. Often at the same high interest rate you just tried to escape.

So the real trade-off isn’t debt vs savings, it’s reducing interest costs vs maintaining access to cash when things go wrong.

What a “good” buffer actually looks like

“Keep a small buffer” is vague. Here’s a more useful way to define it. A minimum buffer should be enough to cover your most likely short-term emergency.

A general rule of thumb for an emergency fund is to cover 3 months' worth of expenses, to also account for job or income loss. If your income is stable and you have other support options, you may need less.

The key is this: Your buffer should reduce the chance that you need to rely on debt again.

A simple system that works for most people

Instead of choosing between debt and savings, use both deliberately.

A practical approach:

- Keep a minimum buffer

- Use the rest of your savings to pay down high-interest debt

- Focus on clearing that debt as quickly as possible

- Once it’s gone, redirect those payments into rebuilding savings

This way, you:

- Reduce interest costs immediately

- Still have access to cash if something happens

- Avoid the cycle of clearing debt and falling straight back into it

Where behaviour matters more than maths

This is the part most people underestimate. You can make the “right” decision on paper and still end up worse off if your behaviour doesn’t support it.

Watch for these patterns:

- Paying off debt, then slowly building it up again

- Keeping savings, but continuing to rely on credit

- Not rebuilding your buffer after using it

A few practical guardrails help:

- Automate debt repayments just after your income comes in

- Keep your savings in a separate account you don’t touch daily

- Avoid increasing your credit limit while you’re paying it down

- Track your total debt balance weekly so you can see progress

This is what turns a one-time decision into something that actually sticks.

Important edge cases to consider

The “pay debt first” approach isn’t universal. Adjust based on your situation.

- If your income is unstable → prioritise a larger buffer

- If your debt is very high → lean more aggressively into repayment

- If you tend to rely on credit → reduce access (e.g. lower your limit)

- If you already have a strong emergency fund → focus fully on clearing debt

The right balance depends on your risk, not just the numbers.

What actually matters

This decision isn’t about choosing the perfect option once. It’s about setting up a system you can maintain over time. You need:

- Enough access to cash to handle life

- To reduce expensive debt that’s working against you

If you get both right, you stop moving in circles and start making real progress.

What this means for employers

Questions like whether to use savings to pay off debt are not just personal finance questions people ask in isolation. For many employees, these decisions sit in the background every day, adding stress and uncertainty that can affect their focus, energy and confidence at work.

When someone is constantly worrying about debt or how they would handle an emergency, it can start to impact their wellbeing, productivity and even attendance over time.

Wealthbit’s Financial Freedom Programme® gives employees tools and guidance to build healthier money habits, reduce financial stress and feel more in control of their finances.

👉 Sign up for Wealthbit's Money Systems newsletter and make financial freedom simple.

Tools that might be helpful:

Debt repayments email course: take control of your debt in 4 days

Debt Repayment Strategies workbook - a practical tool to build a system that works for you

Other resources to explore:

Debt review in South Africa: what it means and how it works

How do I check my credit score for free in South Africa?

What does “blacklisted” really mean in South Africa?

Is it okay to handle debt on your own without telling your partner?

How to get a good credit score in South Africa and why it matters

Should I use my savings to pay off my credit card debt, or continue saving?

Is it bad to only pay the minimum on my credit card?

Snowball vs avalanche: Choosing a debt repayment strategy that fits your personality

Why we fall into debt: the most common causes and how to spot the early signs

.png)

.png)

.png)