Is it bad to only pay the minimum on my credit card?

When money is tight, making the minimum payment can feel like a relief. It helps you stay on top of your account, avoid late fees, and protect your credit record. The problem is that it does very little to reduce the balance itself. So while it may ease the pressure for now, it can also keep debt hanging around for much longer than you think.

In this article, we’ll look at how minimum payments work, why they can end up costing you more, and what you can do to make faster progress.

What is a minimum payment on a credit card?

The minimum payment is the smallest amount your credit card provider requires each month to keep your account active and in good standing. It’s usually calculated as a small percentage of your balance, often between 2-5%, or a fixed minimum amount, whichever is higher.

For example, if you owe R10,000 and your minimum payment is 3%, you would need to pay R300 that month.

This payment keeps your account up to date, but it is important to understand what it is designed to do. The minimum payment is not there to help you get out of debt. It is structured to maintain the balance for longer, increasing the total interest paid over time.

What happens when you only pay the minimum?

When you pay only the minimum payment on your debt, most of your payment goes toward interest rather than reducing the actual balance.

For example, you owe R10,000 on a credit card with an interest rate of 18% per year. That works out to roughly R150 in interest added each month.

If your minimum payment is R300:

- R150 goes towards interest

- Only about R150 reduces your balance

After paying R300, you would still owe roughly R9,850. This is why it can feel like you are making payments but not much progress.

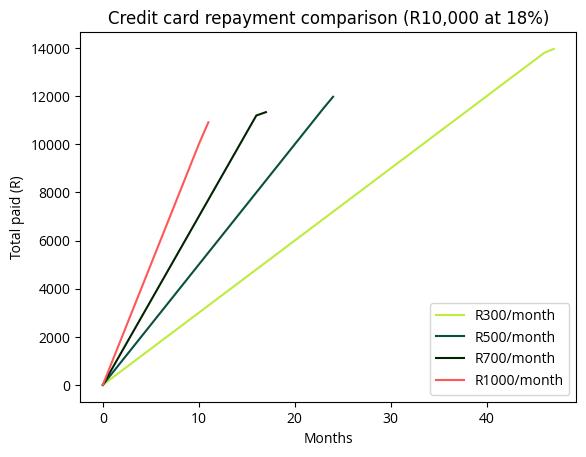

Comparison of repayment outcomes

The difference in repayment outcomes can be bigger than most people expect.

Why paying the minimum can cost you more

- You stay in debt for longer: Because your balance decreases slowly, you can carry the same debt for years.

- You pay more interest over time: The longer the balance remains, the more interest accumulates. In many cases, you end up paying far more than the original amount you borrowed.

- Debt can continue to weigh on you: Long-term debt can affect your financial confidence, limit your flexibility, and contribute to ongoing stress.

Is it okay to only pay the minimum?

There are times when paying the minimum is the only realistic option. Unexpected expenses, tight budgets, or income changes can make it difficult to pay more.

In those situations, paying the minimum is still important. It helps you avoid penalties, extra fees, and negative marks on your credit record.

But paying the minimum is a short-term safety net, not a long-term strategy. It can help you get through a tough month, but it does very little to actually reduce what you owe.

How to understand your debt before making a plan

Before making changes, it helps to get a clear view of your situation. Look at the type of debt you have, the total balance, the interest rate, and how repayments are structured.

Once you can see everything in one place, it becomes much easier to work out what to focus on first and make decisions that help you start bringing your debt down over time.

Why credit card debt needs extra attention

Credit cards typically have higher interest rates than other types of debt. For example, a credit card may charge 18 to 20% interest, while a home loan may sit closer to 10%.

That difference means credit card balances grow faster and cost more to carry. Because of this, credit card debt benefits more than most from being paid off as quickly as possible.

What to do instead of only paying the minimum

- Pay more than the minimum when you can

Even a small extra amount each month can make a meaningful difference. Adding R150 or R200 reduces the balance faster and cuts down the interest you pay over time.

- Focus on one debt at a time

Trying to pay off everything at once can feel overwhelming. A more manageable approach is to keep making the minimum payments on all your debts, while putting any extra money towards one specific debt. That way, you stay on top of your payments and lower the risk of late fees or extra interest.

Two common debt repayment strategies are the snowball method and the avalanche method:

- The snowball method focuses on paying off the smallest balance first, which can give you a quick sense of progress and help you stay motivated.

- The avalanche method focuses on the debt with the highest interest rate first, which can save you more money over time, but it may take a bit longer before you feel like you are making a dent.

- Use minimum payments strategically

Minimum payments help you stay up to date on all your accounts and avoid extra fees or penalties. From there, any extra money you can put aside can go towards the debt you have chosen to focus on first.

That way, minimum payments help you stay on track, while your extra repayments are what start moving things forward.

What this means for employers

Money stress has a way of following people into the workday. When someone is worried about debt, repayments, or simply making it to the end of the month, it can affect their day-to-day performance.

The Wealthbit Financial Freedom Programme® helps employees understand their financial situation, build better habits, and reduce long-term stress.

👉 Sign up for Wealthbit's Money Systems newsletter and make financial freedom simple.

Tools that might be helpful:

Debt Freedom Tool - shows what your debt costs, the best repayment strategy, and your debt-free date

Debt repayments email course: take control of your debt in 4 days

Debt Repayment Strategies workbook - a practical tool to build a system that works for you

Other resources to explore:

Should you change careers to pay off debt faster?

Snowball vs avalanche: Choosing a debt repayment strategy that fits your personality

Why we fall into debt: the most common causes and how to spot the early signs

Debt review in South Africa: what it means and how it works

How do I check my credit score for free in South Africa?

What does “blacklisted” really mean in South Africa?

Is it okay to handle debt on your own without telling your partner?

How to get a good credit score in South Africa and why it matters

Should I use my savings to pay off my credit card debt, or continue saving?

.png)

.png)

.png)